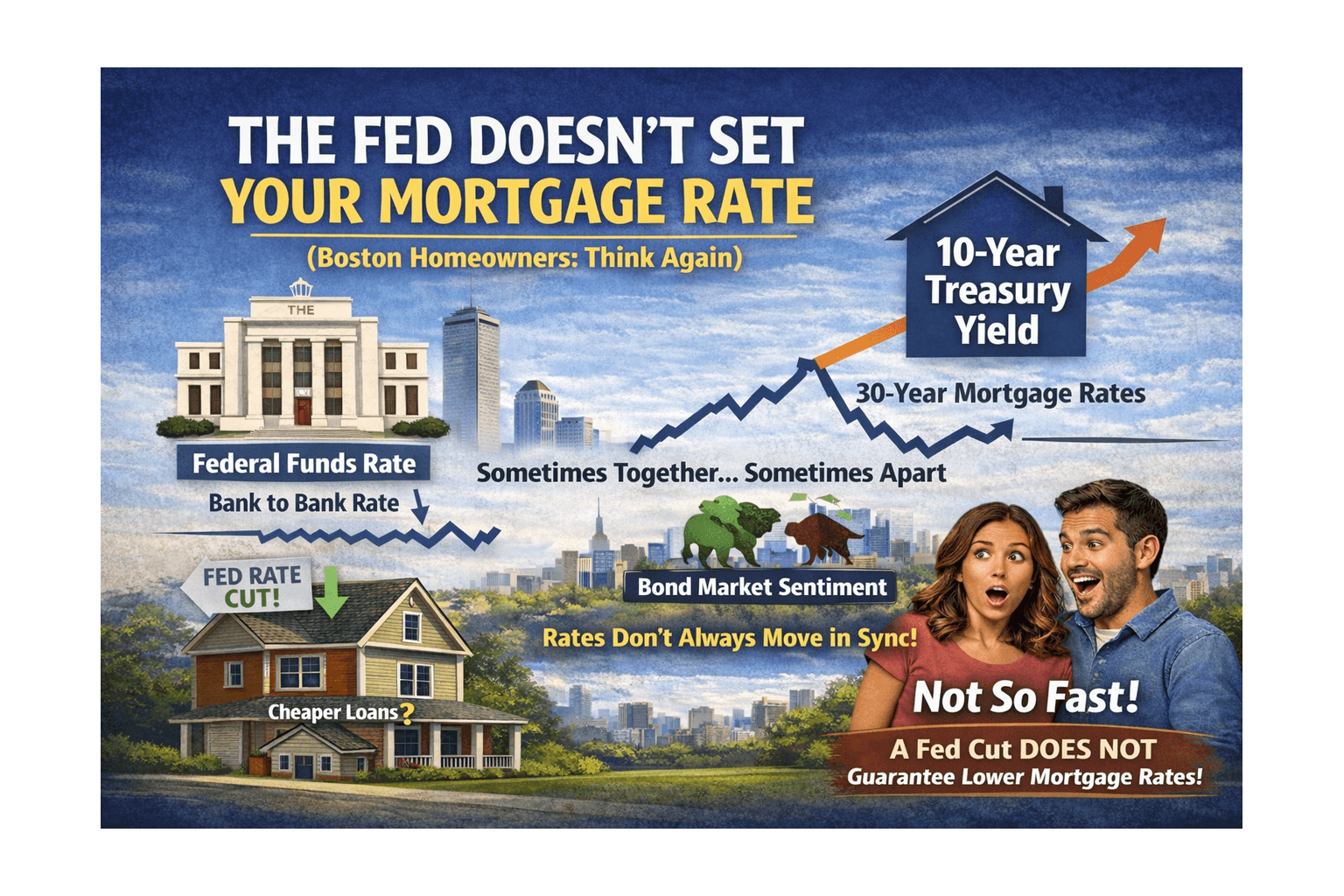

# The Fed Doesn't Set Your Mortgage Rate (Boston Homeowners: Think Again)

Does the Federal Reserve control mortgage rates?

No. The Fed does not set mortgage rates.

Here's what Boston-area homeowners and buyers actually need to know:

The Fed controls the federal funds rate—the overnight rate banks charge each other. Meanwhile, 30-year fixed mortgage rates follow the 10-year Treasury yield. These two rates sometimes move together. Sometimes they don't. They can diverge for months based on inflation data and bond market sentiment.

When someone tells you a Fed cut guarantees lower mortgage rates immediately, they're wrong.

The Myth That Creates Expensive Waiting

Many people assume the Fed has a direct dial controlling monthly mortgage payments.

That assumption breeds "paralysis by analysis"—waiting for a press conference that may not deliver better pricing when you're ready to buy.

What this means for you: Timing a purchase around Fed meeting dates can cause you to miss real negotiating windows that exist regardless of what the Fed does next.

What Actually Moves Mortgage Rates: The Yield Curve

To understand why your mortgage rate doesn't drop the second the Fed Chair speaks, you need one concept: the yield curve.

The Fed mainly controls the short end—overnight rates. This impacts credit cards and HELOCs. The bond market influences the long end, which is where 30-year mortgage pricing lives.

Mortgage lenders price loans based on the risk of holding that debt for decades. Their key benchmark? The 10-year Treasury note.

If investors fear inflation—even while the Fed cuts rates to stimulate the economy—bond yields can rise. Mortgage rates rise with them.

Late 2020 saw record-low rates not just because of the Fed, but because the spread between Treasuries and mortgages was compressed.

Key interest-rate markers (selected dates)

Headline-rate context pulled from cited sources, grouped by period to show how benchmark rates, policy rates, and mortgage rates lined up in late-2020 vs. late-2023, plus the Fed’s stated inflation target.

Dec 2020 (record-low context)

10-year Treasury note rate0.93 percent

Secondary spread0.45 percent

Oct 2023 (cycle-high context)

Mortgage rates (cycle-high)7.8 percent

10-year Treasury note (monthly average)4.8 percent

Federal funds rate5.33 percent

Federal Reserve goalpost

Fed's target2-percent

The "Spread" You Should Watch (Not Just the Fed)

The gap between the 10-year Treasury yield and the 30-year mortgage rate is called the spread.

Historically, the spread runs about 1.7 to 2 percentage points. During volatility, the spread can widen, keeping mortgage rates high even if Treasury yields dip.

December 2020: components shown alongside the 10-year Treasury rate

Side-by-side view of the two percent-based components explicitly listed for December 2020 in the source.

10-year Treasury note rate

Secondary spread

Key takeaway: Don't time your purchase around Fed meeting dates. Instead, watch the 10-year Treasury yield and the spread. When the spread narrows, mortgage rates can improve—even without dramatic Fed action.

The Boston-Specific Reality: A "Buyer Strike" = Leverage

National headlines love a single storyline. Boston real estate rarely follows it perfectly.

Right now, a localized "Buyer Strike" has formed in Greater Boston, driven by rate fatigue. It's showing up clearly in inventory and market-time metrics.

What's happening on the ground

Condo inventory is up significantly—about 57% year-over-year. That's roughly ~480 to ~755 units.

Condos: Active condo inventory in Boston is up approximately 57% year-over-year.

Multifamily: Boston multifamily inventory has surged roughly 71%.

What this means for you: Fewer competing buyers translate into more room to negotiate—especially in segments where listings are sitting longer.

Negotiation Power Is Showing Up in the Numbers

When Days to Offer (DTO) rises, pricing power shifts from seller to buyer.

In Boston, the median DTO has risen ~19% to about 25 days. That shift allows for:

1. Due diligence—more ability to perform full inspections without waiving protections

2. Concessions—increased ability to secure seller concessions Boston buyers can use, like rate buydowns or closing cost credits

Where the Leverage Is (and Isn't): Neighborhood Snapshot

This "Buyer Strike" isn't evenly distributed. It's most visible in luxury and downtown condo markets where inventory is lingering.

Data Table

| Neighborhood | Median Days on Market | Market Status |

|---|---|---|

| Midtown | ~88.5 Days | High Buyer Leverage |

| Fenway | ~46 Days | Moderate Leverage |

| Back Bay | ~42 Days | Moderate Leverage |

| Suburbs | < 15 Days | Seller Advantage |

Mic Drop Insight: "When median days on market shifts from 39 to 47 days, it represents a pricing-power transfer. The market is currently offering careful buyers something they rarely get in Boston—time and optionality."

October 2023: mortgage vs benchmark vs policy rate (cycle-high context)

Compares three percent-based rates cited for October 2023 to show the relationship between mortgage rates, the 10-year Treasury benchmark, and the policy rate at the time.

Mortgage rates (cycle-high)

10-year Treasury note (monthly average)

Federal funds rate

What this means for you: In parts of the city core, you may have something Boston buyers don't often get—time to negotiate terms, not just price.

Nuance Matters: The Single-Family Exception

Mortgage rates vs Fed policy affects property types differently.

This "Fed disconnect" strategy tends to help most with condos and townhomes in the city core.

Suburban single-family is a different world

While Days on market Boston condos are increasing, single-family in desirable suburbs—Newton, Wellesley, Lexington—remains tight.

Single-family prices have climbed over 5% YTD. Condo price growth has slowed to roughly 2%.

Current 30-year fixed mortgage rate snapshots (as cited)

Text-forward table preserving the exact snapshot values (including timestamp) from each source; useful for context without implying a consistent time series.

Average rate on a 30-year mortgage6.09%

Date1/21/2026

30 Yr. Fixed Rate6.20%

Change-0.01%

TimeWed, 3:09 PM

Key takeaway: If you're chasing a single-family "forever home" in a prime suburb, this leverage may not apply the same way. If you're targeting a city condo or multifamily investment, conditions are more buyer-friendly.

The "Stale Listing" Advantage (30+ Days)

The highest leverage tends to show up on listings that have sat for 30+ days.

Fresh listings in "hot" school districts may still spark bidding wars, even in a high-rate environment.

What this means for you: Strategy matters. The best opportunities often come from identifying where demand has cooled—not assuming the entire metro market behaves the same way.

The Cost of Waiting for the Fed

Waiting for a major Fed-driven rate drop can backfire for two reasons:

1) The competition paradox

If mortgage rates drop to the 5.5% range, the "fence-sitters" may return en masse.

That inventory advantage you have today—including that 57% condo surplus—can vanish. Bidding wars can return. You might get a better rate, but pay a higher price and lose contingencies.

2) The refinance option

You can refinance a high rate if rates drop. You cannot renegotiate the purchase price after you buy.

Actionable Guidance (Boston Edition)

Ignore Fed headlines as a direct predictor of mortgage rates.

Track the 10-year Treasury yield and the spread for rate direction.

Buy for the asset, not the rate—especially while inventory and negotiation leverage are improved.

Negotiate hard: repairs, closing costs, and price reductions can be more achievable in this environment.

Bottom Line

Does the Fed control mortgage rates? No. The market does.

And in Boston, today's market is offering something rare: more leverage and more breathing room in specific segments—especially condos and multifamily.

Call to Action (High-Value Next Step)

If you want, share (1) the neighborhood(s) you're targeting and (2) whether you're looking at condo, multifamily, or single-family—and I'll help you interpret what the current inventory, DOM/DTO dynamics, and rate mechanics mean for your exact purchase timing and negotiation plan in Greater Boston.